Golf course appraisers are often asked the question, “so, what are golf courses selling for these days?”. There are all kinds of answers to that question. There’s one golf course brokerage firm that publishes findings every year on the average sale price of golf courses for the past year. Buyers of golf courses, especially the more active ones will often quote a gross revenue multiple that coincides with their investment objectives and desires. The Society of Golf Appraisers annually publishes an Investor Survey that provides information on gross revenue multipliers and other metrics that measure the pulse of the industry on certain benchmark indicators like capitalization rates, discount rates, mortgage terms and other indicators.

What these transactions tell us provides appraisers and market participants alike the ability to compare sales of different golf facilities on the basis of a common denominator that helps the market determine value and those of us that do appraisals reflect their behavior in developing our opinions of value. Just as important, however is what sales DON’T tell us.

The gross revenue multiplier (GRM) largely became useful when more and more golf courses fell into distress. Since many golf properties had little or no cash flow, extracting a capitalization rate by simply dividing cash flow by the sale price yielded distorted results. Many of the properties that sold weren’t/aren’t stabilized and especially when a property had negative cash flow sales didn’t tell us much. Many purchasers now rely on historical gross revenues to assist in making purchase decisions. What these multiples don’t tell us are the following:

- What the cash flow situation is

- Whether the property is stabilized

- How much capital investment the property might need

Each of these factors impact the GRM and understanding the sold club’s history can help interpret the GRM for application to the property being appraised. Annually, there is a survey published that analyzes the dollar sale prices of golf properties sold during that year. While an interesting metric, the average sale price doesn’t reveal much about the economics of the golf course industry. Recently, we at Golf Property Analysts reviewed and analyzed the sales we’ve researched over the past few years for our various assignments and learned a considerable amount about the market.

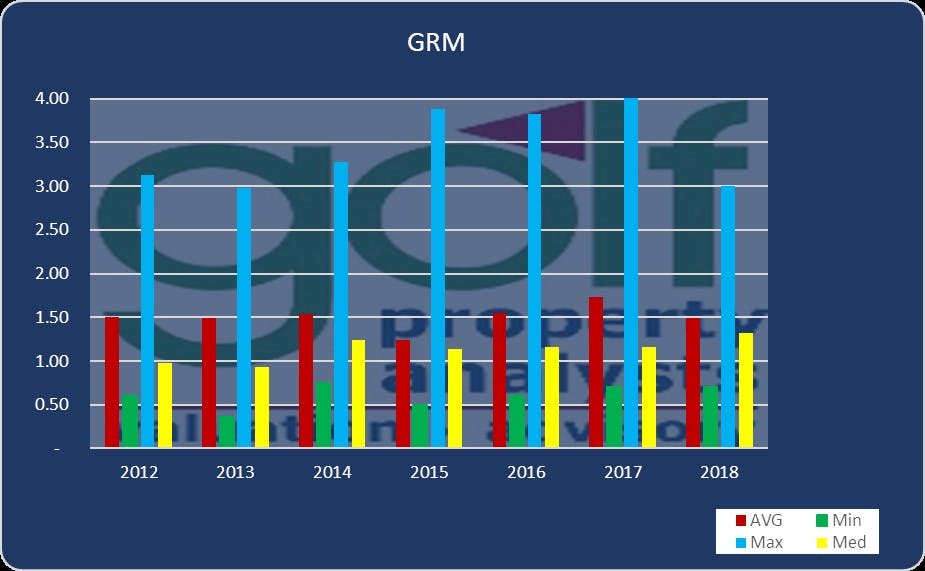

Our research included nearly 200 sales of golf properties in about 20 states which occurred in the past 5 years. The trends are enlightening. Sale prices don’t show any appreciable trends. They seem to move up and down significantly enough that no stable trend can be identified. A few very high priced or low priced sales can impact the statistics too much for reliable use. Conversely, studying Gross Revenue Multipliers (GRM) shows pretty remarkable consistency over the broad brush view of so many sale transactions.

The average GRM has stayed pretty consistent around the 1.5 mark for the past 6 years, which is consistent with market interview surveys and the SGA survey. Additionally, the median has hovered from just below 1.0 to nearly 1.5 with extremes of less than .5 and more than 3.0. These #’s are illustrated in the adjacent graphic. Our next step is to explore the different trends between daily-fee and private facilities and see if there are differences. Certainly, these different operating models attract different buyers. The question is whether their investment criteria are similar.

Above all else, this tells us that economics largely drive the purchase of golf properties. Yes, there is the occasional “hobbyist” that can afford to and wants to buy golf properties, and there are other metrics besides GRM. The most logical metric among them being the overall capitalization rate or cash flow multiple. The problem is that indices calculated on net cash flow are often distorted by the fact that many golf courses experience limited or even negative cash flow, but still have value, either because they’re not well-managed, aggressively marketed or properly positioned in the marketplace.

When valuing a property, some conclude that the GRM is simply the averages shown and this can be misleading. A more focused analysis on the most relevant sales for a given property is required, and even a .25 adjustment one way or the other from the seeming trend of averages hovering around 1.5 can make a big difference. A .25 adjustment in the GRM on gross revenues of $4 million can alter the value by $ 1 million.

Comparable sales can tell us a lot about the value of any golf property. However, it is imperative that appropriate units of comparison (GRM in today’s world) be used and that relevant (truly comparable) sales be analyzed in each case.